Daily Market Outlook, November 11, 2020

.png)

Daily Market Outlook, November 11, 2020

Risk tone remained mostly positive, with equities outperforming in sectors such as travel and leisure that would benefit from a potential breakthrough in a coronavirus vaccine. In contrast, sectors that profited from lockdown restrictions, such as technology, underperformed, not helped by reports of China increasing regulation on the industry. Nevertheless, while an effective vaccine would be a game-changer, more testing is still needed. In the meantime, global Covid-19 cases and fatalities are likely to continue to mount this winter.

There is little in the way of economic data releases today, but UK GDP figures will be released at 7am tomorrow. The September figures will complete the picture for Q3. Growth in August slowed to 2.1%m/m, despite the boost to the accommodation and food services subsector from the Eat Out to Help Out scheme. That compared with increases of 9.1% and 6.4% in June and July, respectively. Expect September GDP to have risen by 1.9%, similar to the August outturn, which would result in a record rebound of 15.9%q/q in Q3 after the 19.8% slump in Q2. The output for UK GDP in Q4, however, has darkened following the rise in coronavirus infections and the reintroduction of containment measures in England. The Bank of England now expects the economy to contract again in Q4, although growth is expected to resume in 202. The risk there is if more severe or longer-lasting lockdown restrictions are put in place. Conversely, faster medical advances such as a vaccine present upside risks to the outlook.

News this week of a potential breakthrough in a vaccine is a case in point, raising hopes of a return to normal by the spring, although the vaccine is not expected to be widely available to deal with this winter’s second wave. ECB President Christine Lagarde will give an introductory speech at 1pm on the first of a two-day online ECB Forum on Central Banking, which will look at issues such as deglobalisation, climate change and policy challenges. Her speech will be followed by sessions chaired by Vice-President Luis de Guindos and Chief Economist Philip Lane. Ms Lagarde will also take part in a policy panel on day two of the Forum (tomorrow) along with US Fed Chair Jerome Powell and Bank of England Governor Andrew Bailey.

Today’s Options Expiries for 10AM New York Cut

- EURUSD: 1.1770-80 (830M), 1.1810 (778M), 1.1830-35 (1.1BLN)

- USDJPY: 104.00 (550M), 105.30-35 (600M)

- AUDUSD: 0.7320 (213M)

Technical & Trade Views

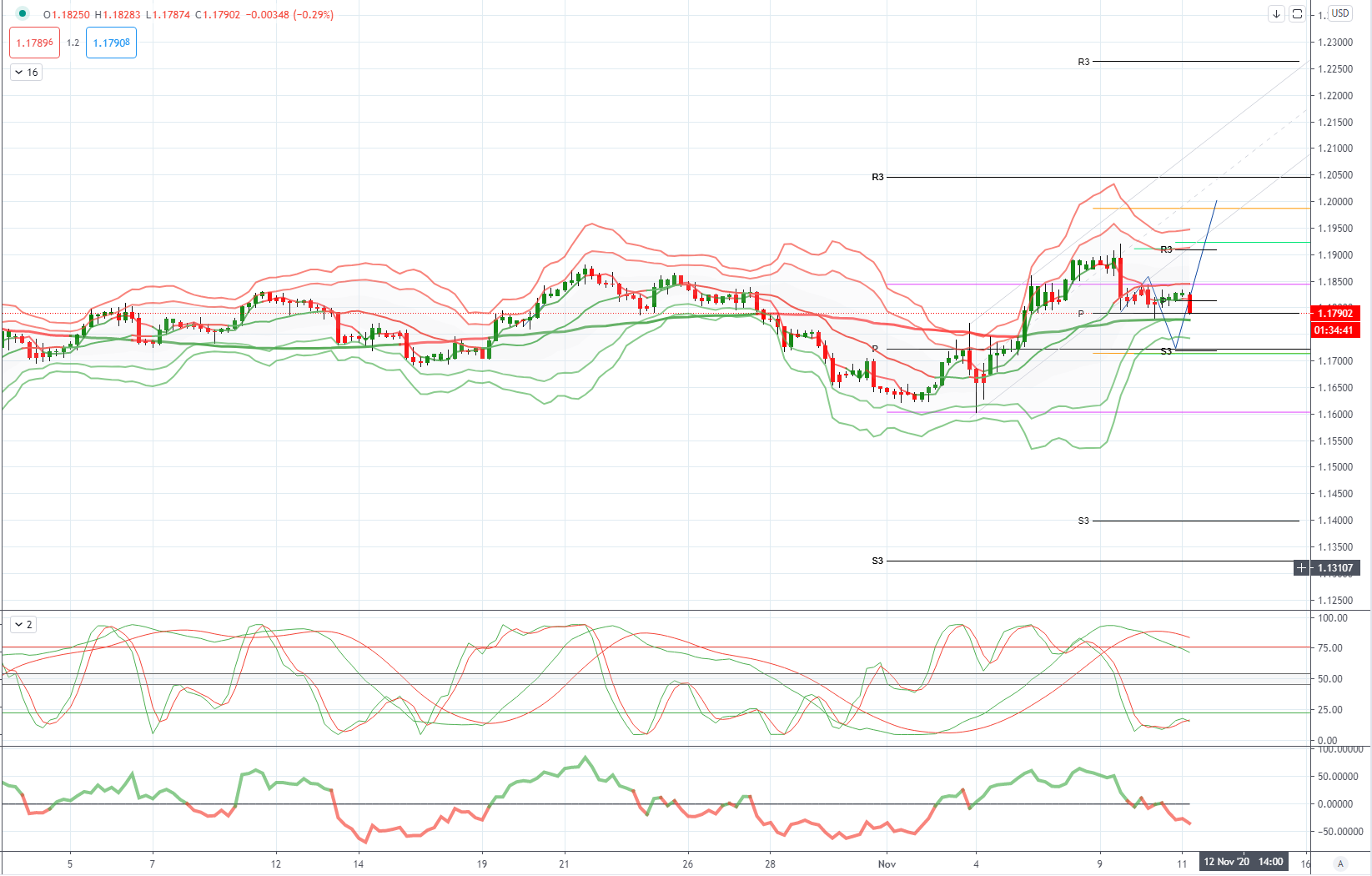

EURUSD Bias: Bullish above 1.1750 bearish below

EURUSD From a technical and trading perspective, as 1.1750 acts a support look for a retest of cycle highs at 1.20, failure below 1.1750 opens a retest of range support at 1.16

Flow reports suggest topside offers through to the 1.1920 level, even there where you’re likely to see weak stops you will find the same type of congestion continuing to the 1.1950 before weakening a little and increasing for any move to the 1.2000 level. Downside bids light through the 1.1800 area with weak stops on a dip through the 1.1780 area and opens the market for a renewed challenge of the 1.1700 area with light support from there.

GBPUSD Bias: Bullish above 1.2861 targeting 1.3266

GBPUSD From a technical and trading perspective, while 1.2950 attracts sufficient bids look for a test of primary equality objective at 1.3264 UPDATE target achieved

Flow reports suggest topside offers into the 1.3300 level are likely to be a little light with limited congestion through to the 1.3400 level before stronger offers start to appear with weak stops on a break through the level to open the 1.3500 level for a second test of the year. Downside bids light back through the 1.3200 level with congestion forming around the 1.3150 and stronger to the 1.3100 level, weak stops on a move through the area and nothing special until the 1.3000 one suspects

USDJPY Bias: Bearish below 104.30 bullish above

USDJPY From a technical and trading perspective, as 104.30 supports look for a test of descending trendline resistance at 105.50 UPDATE as 104.30continues to attract buyers look for a breach of 105.50 to open a test of 106 next

Flow reports suggest downside bids light through the 104.50 level before beginning to thicken on any dip below the 104.00 level increasing on move through the 103.50 level with weak stops likely on a dip through the 103.00 area with the stops likely to increase through 102.80, topside offers likely to increase through to the 106.00 area with weak stops through the 106.20 area and increasing congestion on a push above the 106.50 level and into the 107.00.

AUDUSD Bias: Bearish below .7243 bullish above

AUDUSD From a technical and trading perspective, as .7240/20 now acts as support look for a retest of offers and stops above .7400

Flow reports suggest topside congestion through the 0.7300 area and likely to continue through to the 0.7320 area before a little less resistance through to 0.7350, however a push through this level is likely to see increasing offers into the 0.7380 level and continuing through to the 0.7420 and the highs since September, strong breakout stops likely on a move through the level and opening a larger move higher against the rub of the economics for the moment. Downside bids light through to the 0.7140 level before finding some light congestion with stronger bids into the 71 cents level to some extent however weak stops and then better bids through the 0.7050 area and increasing into the 70 cents level with short term profit taking likely.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% and 75% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!