Institutional insights: Deutsche Bank USD & Oil

Why the USD Is Undershooting Oil

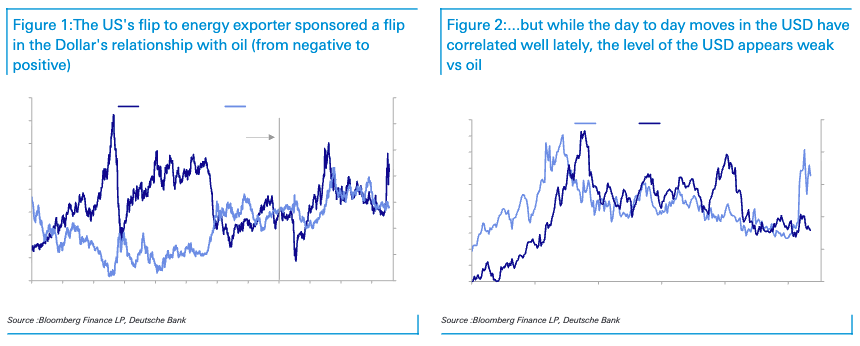

The USD has become positively correlated with oil since the US shifted from being a net energy importer to a net oil and gas exporter. In theory, higher oil should now support the dollar through an improved US terms of trade. That relationship has broadly held during the US-Iran conflict: day-to-day moves in oil and the dollar have been positively correlated. But the level of the USD still looks low relative to the size of the oil move.

The core explanation is that oil is helping the USD, but not enough to offset other drags. Rate differentials, muted US terms-of-trade improvement, LNG bottlenecks, rising import prices, and structural diversification concerns are all limiting the dollar’s upside.

## Main message

The USD is not ignoring higher oil. It is responding to it, but the response is smaller than expected because the oil shock has not translated into a large improvement in US export prices or the broader US terms of trade. At the same time, the dollar’s traditional support from rate differentials is weak, while structural concerns around reserve diversification, global invoicing, and the US security umbrella continue to weigh on sentiment.

So the dollar looks around 2% cheap on a DXY basis versus a basic model using oil and rate spreads, but the undershoot is explainable.

## 1. The USD/oil relationship has flipped

Historically, higher oil was usually negative for the USD because the US was a major net energy importer. Higher oil worsened the US terms of trade, raised import costs, and transferred income abroad.

That changed as the US became a net oil and gas exporter. Higher energy prices now have a more positive impact on the US external position, so the dollar’s correlation with oil has flipped from negative to positive.

This explains why the dollar initially benefited from the US-Iran conflict and why daily moves in oil and the USD have correlated well recently. But the level of the dollar still appears weak relative to oil.

## 2. Rates explain much of the undershoot

The first reason is rates. The dollar is not driven by oil alone. It is also highly sensitive to relative yields, and the dollar’s yield support has been near multi-year lows.

Including rate spreads alongside oil in a simple USD model explains much of why DXY is not higher. In other words, oil is pushing the dollar up, but weak relative rate support is pulling it down.

That said, even after accounting for rates and oil, the model suggests the dollar is still roughly 2% cheap on a DXY basis. So rates explain a lot, but not everything.

## 3. The terms-of-trade boost has been smaller than expected

Oil supports the dollar mainly through the terms of trade: the ratio of US export prices to import prices. If energy export prices rise faster than import prices, the US terms of trade improves, supporting the currency.

But this time, the terms-of-trade improvement has been modest. US terms of trade only moved marginally higher in Q1, unlike the much larger 5-6% increases seen in Q1 and Q2 2022 after Russia’s invasion of Ukraine.

That is the key difference. The oil price has risen, but the US has not captured as much of that price increase through export prices.

## 4. LNG bottlenecks are limiting the export-price benefit

A major reason is natural gas. US export prices have undershot what would normally be expected given the oil move. One important drag is LNG.

Even though European and Asian natural gas prices have risen because of the US-Iran war, US domestic natural gas prices have eased due to a domestic supply glut. US pipelines are full, and LNG export facilities are already near capacity, meaning cheap US gas cannot fully reach overseas buyers.

So the US is not receiving the full global gas-price benefit. This weakens the export-price channel and limits the terms-of-trade support for the dollar.

In simple terms: the US has the gas, but not enough export capacity to monetize the global price spike.

## 5. Import prices are rising again

The second reason the terms-of-trade boost has been muted is that US import prices have been rising strongly.

Import prices are measured before tariffs, and non-fuel import prices have risen 2.8%, the strongest pace since October 2022. Capital goods prices are especially firm, growing at one of their strongest rates since the early 1990s.

This may reflect the AI capex boom showing up in import prices. US imports of AI-related products have reportedly grown sharply since 2023, far outpacing non-AI import growth. Since capital goods are only around 30% of the overall import price index, the headline index may even understate the true import-price pressure from AI infrastructure demand.

This matters for FX because rising import prices offset the export-price gains from energy. So even if oil is higher, the net terms-of-trade benefit is smaller.

## 6. Tariffs appear to be paid by US importers, not foreign exporters

The behavior of import prices also has an important tariff implication. If foreign exporters were absorbing the cost of US tariffs, US import prices should have fallen. But they have not.

Instead, import prices have continued to rise, suggesting that US importers, businesses, and consumers are bearing much of the tariff cost. That is consistent with the idea that tariffs are functioning more like a domestic cost shock than a foreign exporter margin shock.

For the dollar, this is not straightforwardly bullish. Tariffs may reduce imports over time, but if they raise domestic prices and squeeze consumers or businesses, they can also become a growth and inflation problem.

## 7. Prices versus volumes: the US may still benefit through export quantities

The fact that terms of trade has not risen much does not mean the US trade balance is not benefiting from the conflict.

The note makes an important distinction between prices and volumes. The terms-of-trade analysis focuses on prices. But the US may still benefit from higher export volumes if buyers divert energy demand away from the Middle East and toward US suppliers.

So the US may gain via export receipts and volumes, even if export prices do not rise as much as expected. That helps the external balance but may not support the dollar as directly as a sharp terms-of-trade price improvement would.

## 8. Other structural and cyclical USD drags remain

Beyond rates, oil, and terms of trade, several broader factors are weighing on the dollar.

First, the shape of global yield curves has become more supportive outside the US. It is not just the level of rates that matters; slope and curvature now look more favorable for some non-US currencies.

Second, central banks may be selling US Treasuries to support intervention efforts. That can weigh on dollar sentiment and reduce the automatic reserve-demand support for USD assets.

Third, there are structural concerns around the US security umbrella and the dollar’s long-term role in global invoicing. If geopolitical fragmentation leads countries to diversify reserves, trade settlement, or invoicing away from the dollar, that becomes a persistent USD headwind.

These structural forces are slow-moving, but they help explain why the dollar has not fully responded to oil the way a simple energy-exporter framework would suggest.

## Trading implications

The dollar should remain positively exposed to oil as long as the US energy-exporter regime remains intact. But the relationship is not one-for-one. Higher oil is supportive, yet the upside is capped if rate differentials are weak and the terms-of-trade improvement is limited.

The cleanest bullish USD setup would require:

- Oil remaining high or moving higher

- US export prices rising more clearly

- LNG bottlenecks easing or global gas prices feeding into US export prices

- US rates outperforming foreign rates

- Less concern around reserve diversification and global invoicing

- Import-price pressure easing

The bearish USD risk is that oil remains high but continues to act more like a domestic inflation tax than a clean terms-of-trade boost. If import prices keep rising, tariffs squeeze consumers, and the Fed is trapped between inflation and slowing growth, the dollar may continue to undershoot.

The USD is undershooting oil because the oil shock has not delivered the same terms-of-trade windfall as in 2022. US export prices have not risen enough, partly because LNG export constraints prevent the US from fully capturing higher global gas prices. At the same time, US import prices are rising, likely helped by tariffs and AI-related capital goods demand.

Rates also matter: the dollar’s yield support is weak, and broader structural concerns remain a drag. While the USD’s positive correlation with oil remains intact, higher oil prices alone do not suffice to strengthen the dollar significantly. The result is a dollar that looks modestly cheap versus oil and rates, but not inexplicably so.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!